As a buyer, one of the most important questions (if not the most important), that we ask ourselves is “how much house can I afford?” We wonder if we can truly afford the dream home in the picture perfect neighborhood we aspire to have.

Asking yourself about your budget upfront can help you in avoiding wasting time on properties that are beyond your limits. While everyone’s budget will vary, there’s a few components that will help you determine your sweet spot!

Put simply, in order to answer the big question of ‘how much house can I afford’ you have to break down:

Your Income (and your significant other/co-buyer)

Your Current Expenses

Once you go through these points, you’ll have much more clarity on the magic number that’s perfect for you!

Your Income

First thing’s first, take a long, HARD look at your current income. Most people look at their on paper salary to determine their budget, but realistically you need to dig deeper than that.

When going about deciding on a budget, it’s best to find your NET income after taxes, fees, insurance and more.

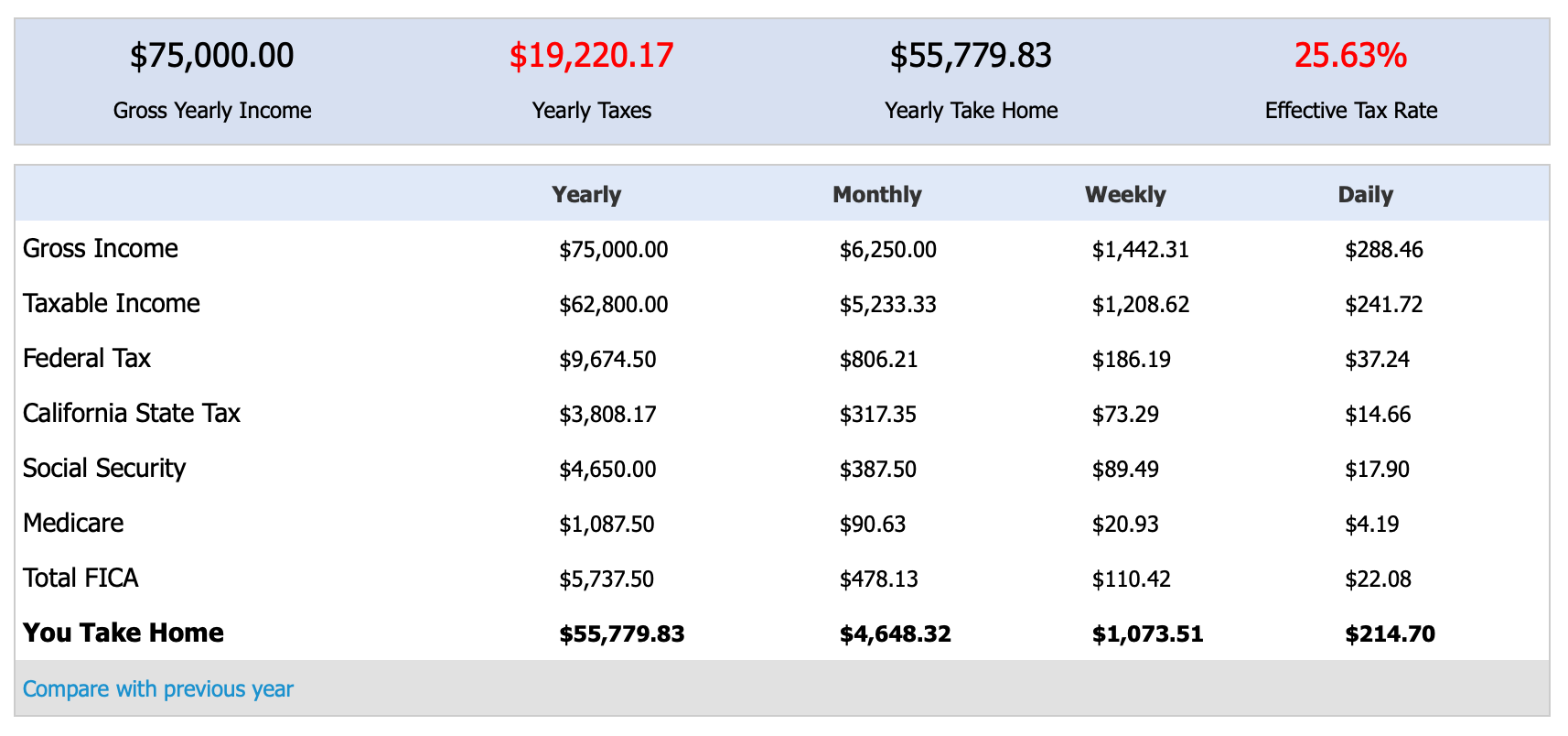

Why is this important? Realistically, if you make $75,000 salary you may only be taking home a fraction of that as “income”. Below shows an example of how that salary really breaks down to just under $56,000 annually which is a BIG difference.

With a $20,000 difference in take home income, you can see why it’s so important to use the net value over the gross! So assess your finances and find out what your immediate income is prior to paying any outside expenses.

Your Expenses

Now that you’ve determined your income, focus on your current expenses. Outstanding debts, auto loans, credit cards, etc. should all be written out here.

Understanding how much money is currently coming in and then subtracting your current expenses will give you the bottom figure of what’s left over.

So…How Much House Can I Afford?

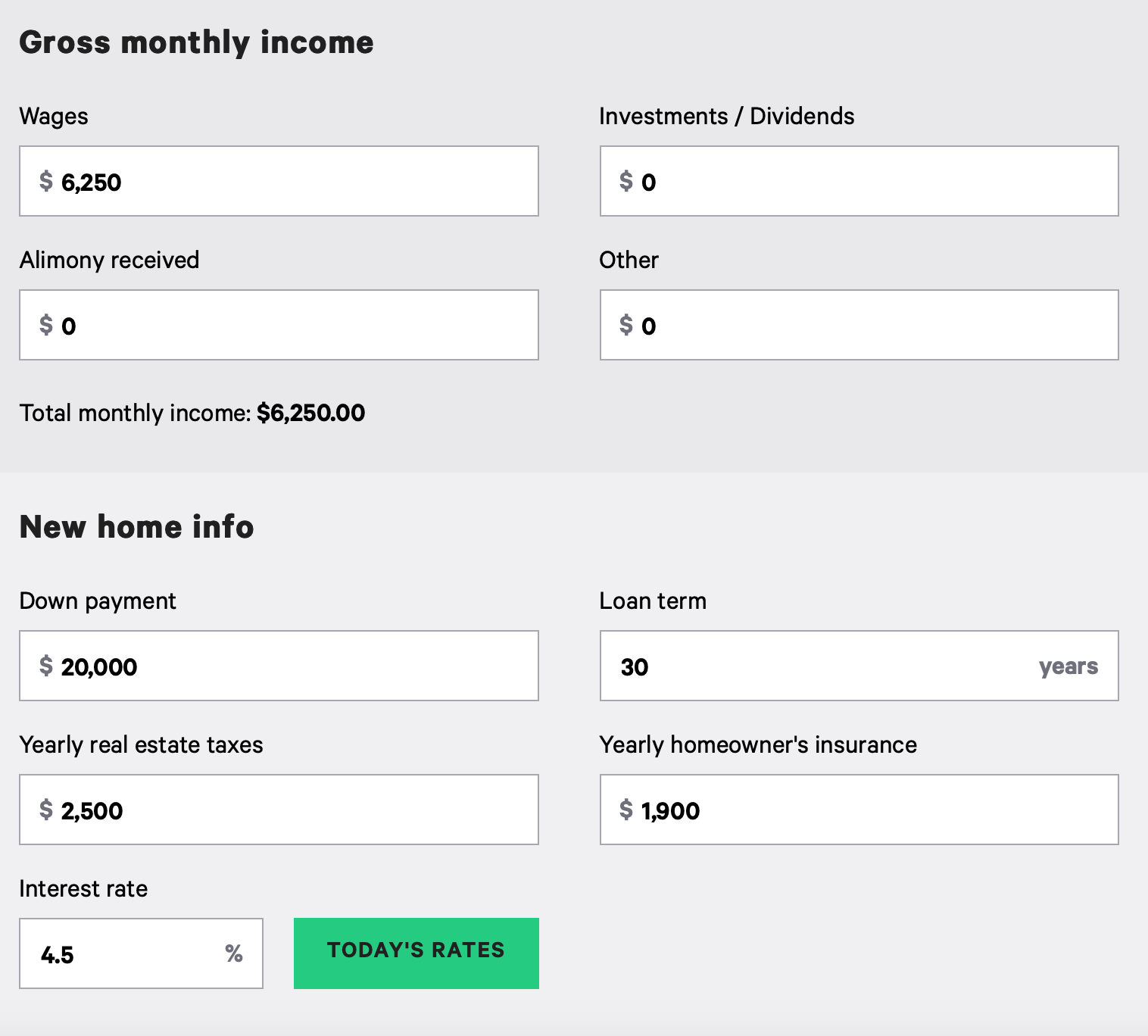

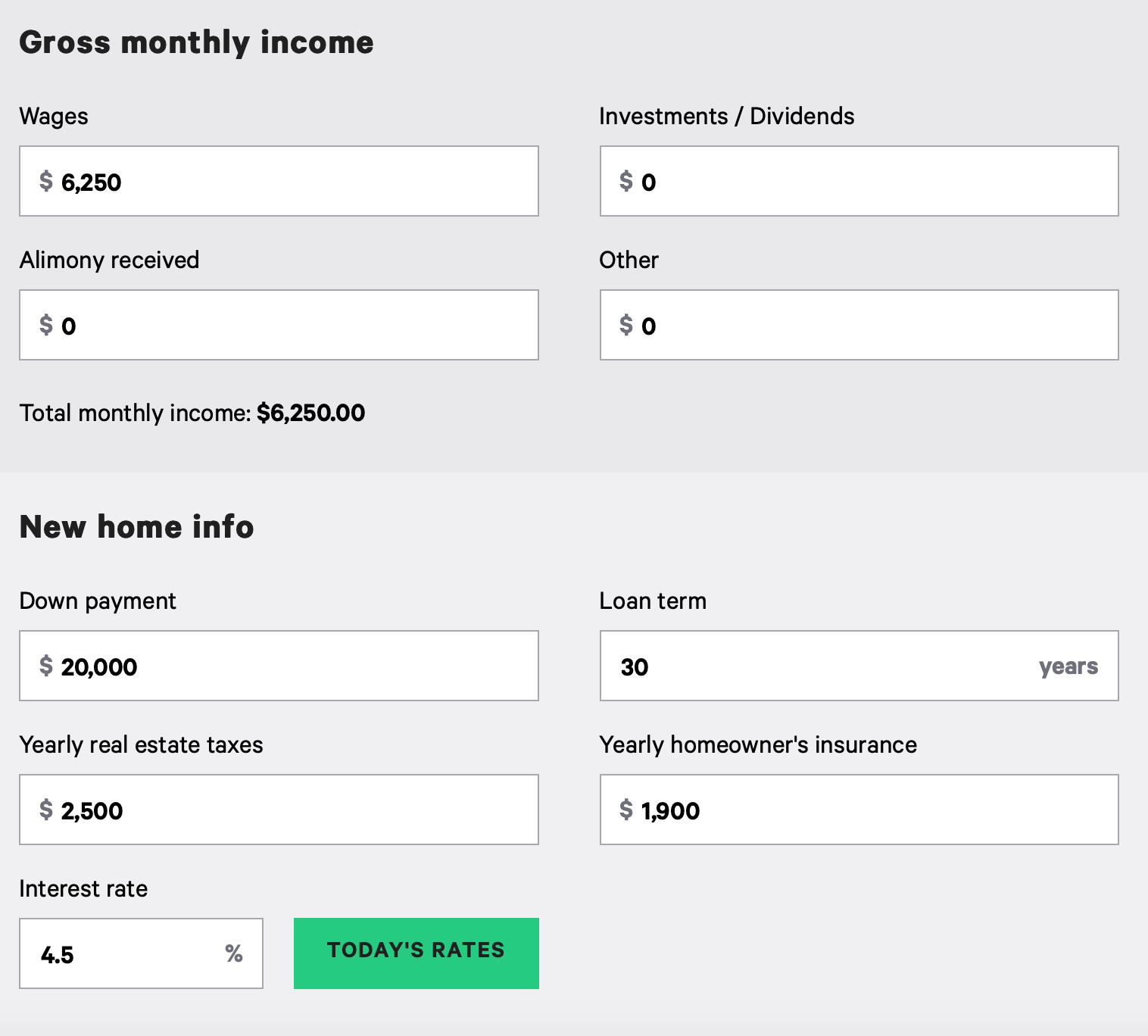

As mentioned on Bankrate.com, the rule of thumb is to spend no more than 28%-30% of your gross income on home expenses. Going back to the above salary of $75,000, if you were looking for a 30 year fixed mortgage that gross salary would give you a suggested budget of $293,016.27 for a home and a monthly mortgage of $1,750 PRIOR TO EXPENSES.

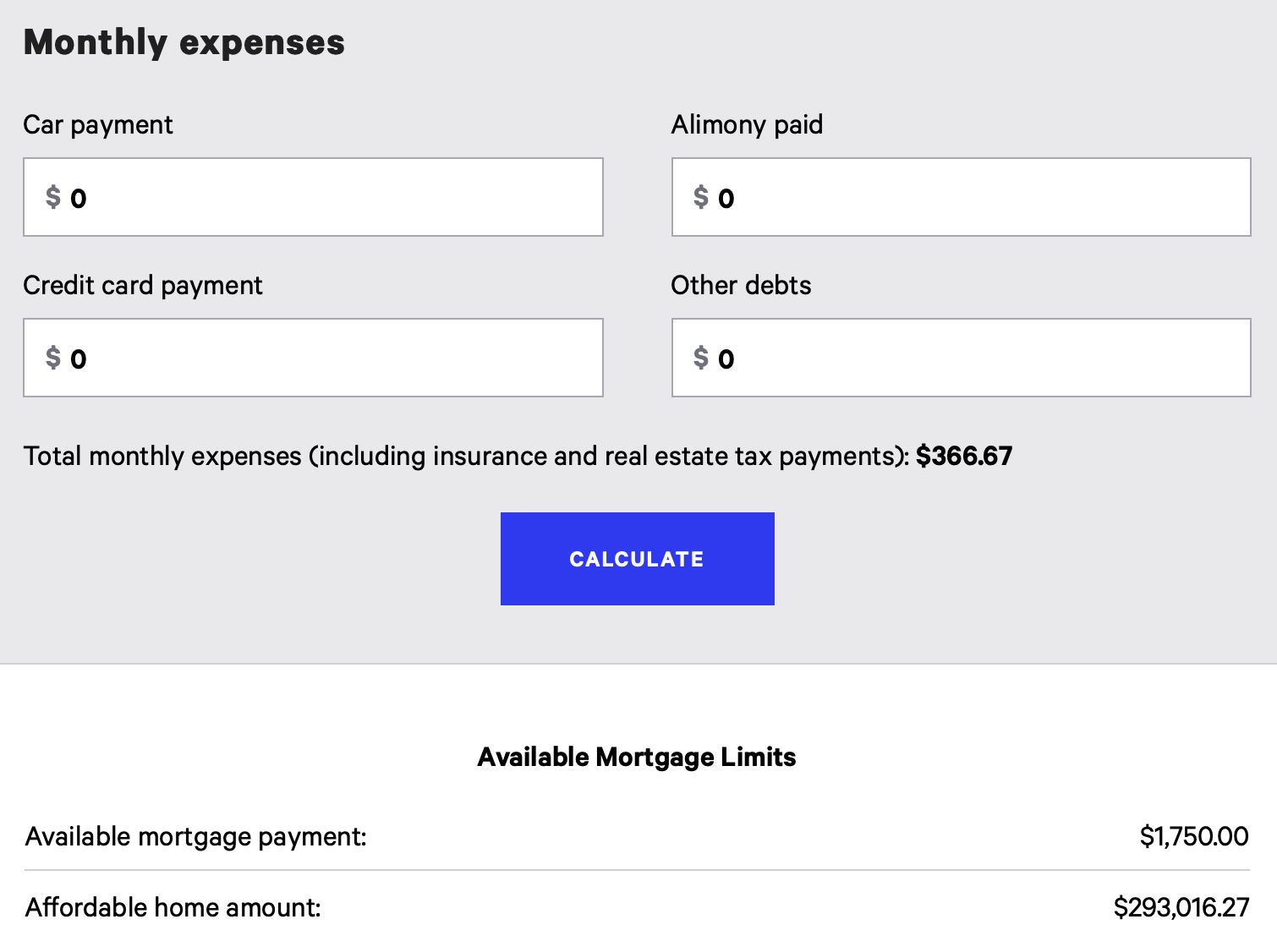

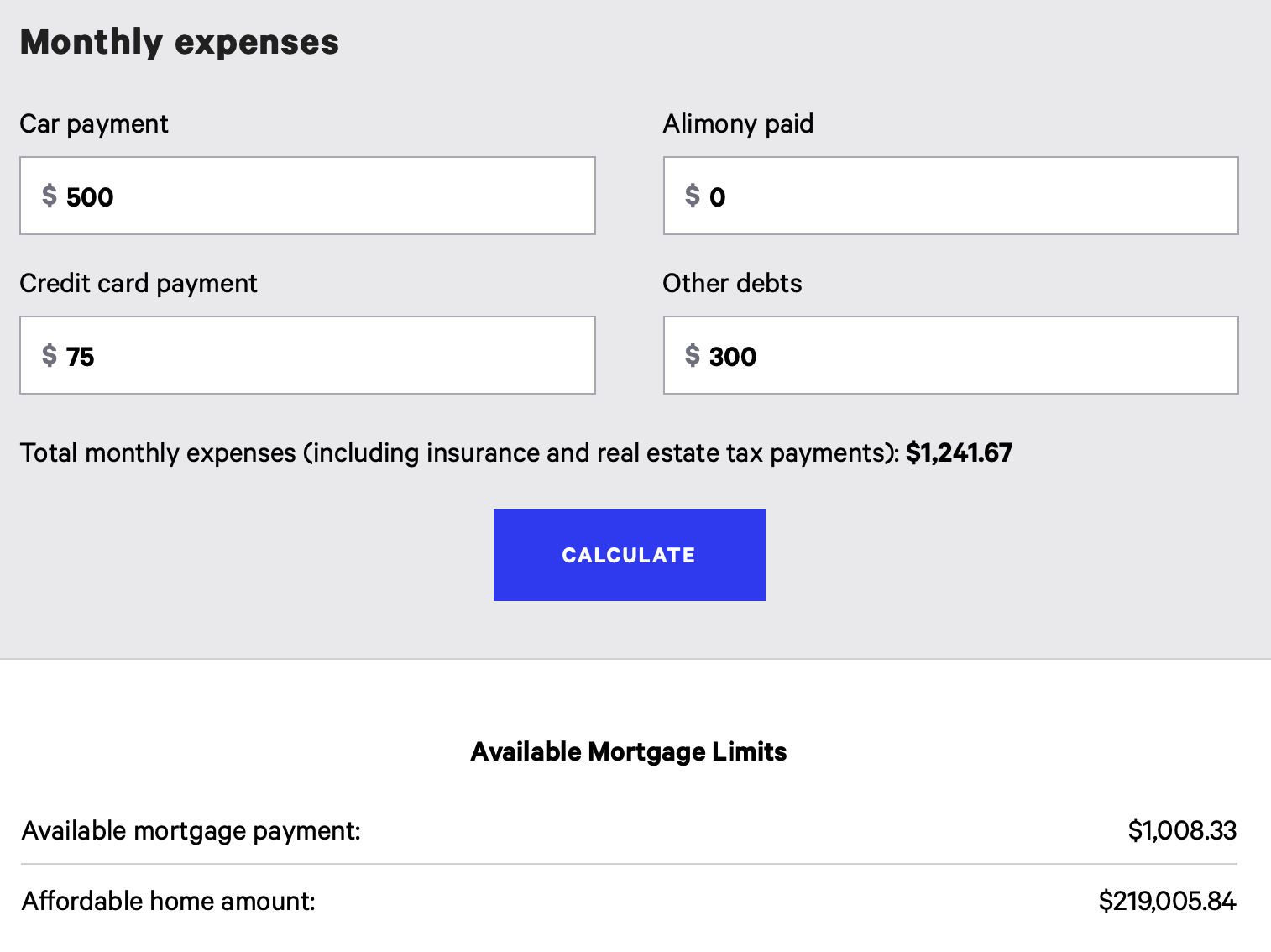

The problem with ONLY doing a percentage of your gross income is it doesn’t allot for other debts you have. If you had a $500 car payment/insurance, $75 credit card payment and $350 student loan payments per month, this shifts your buying power. You’d now have a suggested budget of $219,005.84 for a home and a monthly mortgage of $1,008.33.

Need extra help?

Head over to Bankrate to use their mortgage calculator once you have an idea of your income and expenses. It will calculate your limits just like the photos listed above so you can be confident in your budget.

Need A Realtor In The Bay Area?

Connect with our team today to learn more about available homes in all of the Bay Area.